RETIREMENT INCOME FRAMEWORK

Retirement Income Planning deals with the following issues:

The timing of claiming Social Security benefits

Figuring out whether you have enough money for your retirement

Partial Roth Conversion strategies to enhance retirement wealth by optimizing taxes

How to do the actual retirement transition

Planning for Medicare and out-of-pocket expenses during retirement

Long Term Care planning and impact analysis on the “Retirement Income Roadmap”

Augmenting guaranteed income sources by adding annuities to ensure income to the surviving spouse

Coordinating the liquidation of the retirement accounts and brokerage accounts to replace their paycheck and sustain retirement spending

It is never too late to plan for retirement; however, the sooner planning starts, the more financially prepared you will feel when it arrives. Specialized guidance and support from a CFP® professional can help you develop a plan that delivers a secure and comfortable retirement and peace of mind during your pre-retirement years. Together, we will:

Review expenses that will or are likely to be incurred during your retirement, and create a plan to eliminate any shortfall between income and expenses.

Identify the primary sources of retirement income you have or should have and calculate the savings required to retire at a specific age and achieve your desired lifestyle.

Create strategies for preserving and growing retirement account balances and determining distribution amounts.

Recommend a diverse range of tax-efficient financial tools — IRAs, 401(k)s, investments, and tax-sheltered opportunities — that are best suited to your age and retirement time frame.

Develop a backup plan that responds to unpredictable and unfortunate events, such as death or disability, which can undermine even the best-laid retirement plans.

Accumulation vs. Decumulation phases

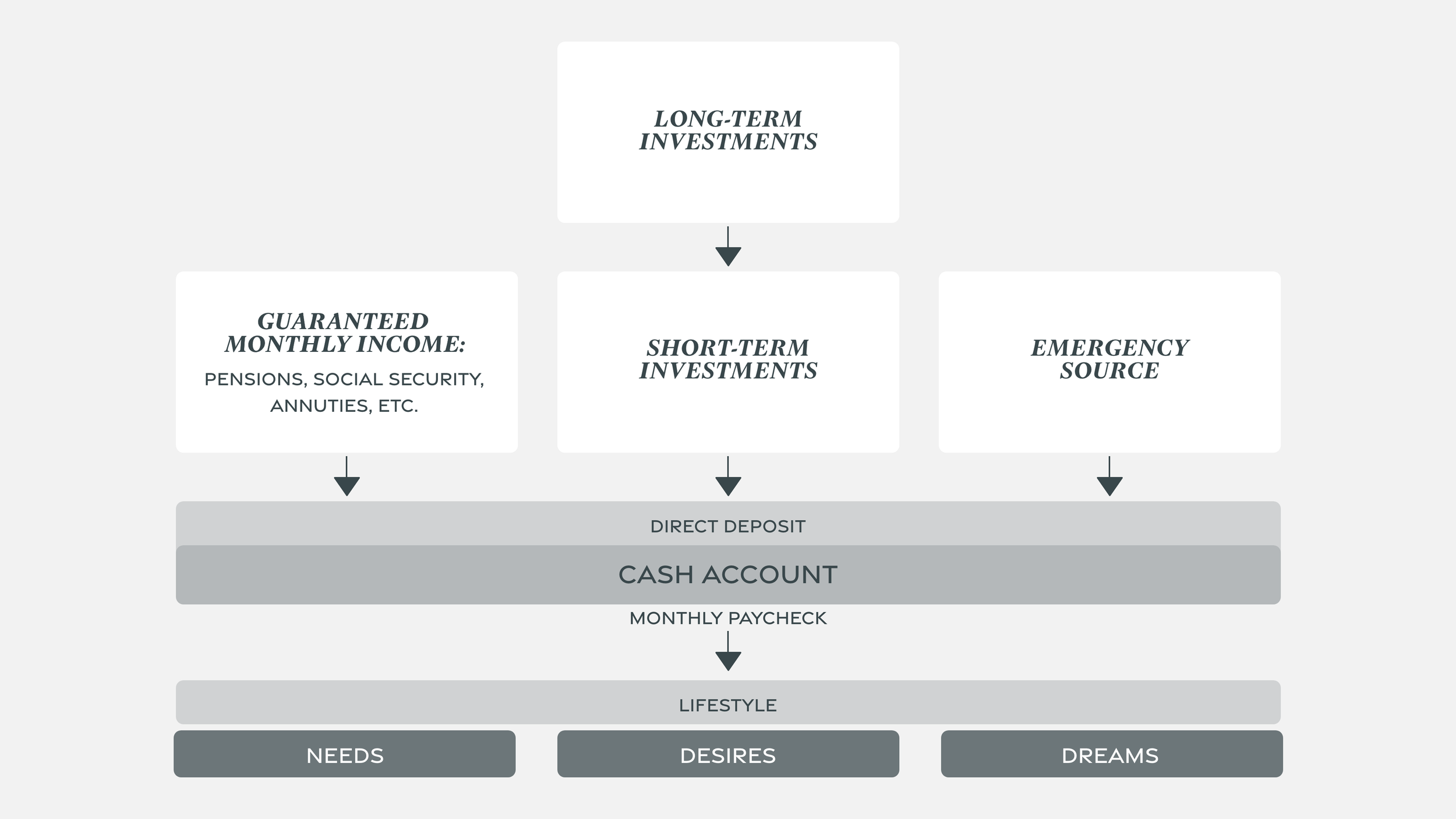

Almost everybody has spent their working lives in the “Accumulation” phase. They are used to a regular source of income which they get every month. After the retirement transition is done, the decumulation phase begins. The monthly paycheck stops, and it has to be replaced by guaranteed sources of income (e.g., Social Security, annuities with income, bond ladders) & regular drawdowns from retirement and brokerage accounts.

Challenges and Risks around the transition to retirement

Sequence of returns risk

Sequence of returns risk is the danger that the timing of withdrawals from a retirement account will have a negative impact on the overall rate of return available to the investor. This can significantly impact a retiree who depends on the income from a lifetime of investing and is no longer contributing new capital that could offset losses.

Bear market at retirement

Account withdrawals during a bear market are more costly than the same withdrawals in a bull market.

Dollar-cost averaging works in Accumulation. However, constant dollar withdrawals in a down market at retirement pose significant risks to the retirement portfolio.

Possible Solutions

During your life's “Accumulation” phase, you need to save and invest efficiently over time. “Decumulation” refers to the de-accumulation of assets in order to maintain your quality of life in retirement. It’s much more complex than the accumulation of assets.

During Decumulation, we need to:

Set up lifetime income sources like Social Security, pensions, and annuities.

Organize your investment portfolio strategically to optimize tax efficiency. This involves withdrawing funds in a tax-savvy manner from taxable, tax-deferred (such as 401K and IRA), and tax-exempt (like Roth) assets. Additionally, effectively manage required minimum distributions (RMDs) in consideration of marginal tax rates.

Covering your health care costs (pre-Medicare and post-Medicare) and long-term care.

Decide whether and when you should tap other sources of wealth like home equity.

Develop solutions that can provide spending confidence—for both essential spending needs and more discretionary “wants.”

Insurance solutions can play an important role in an integrated retirement income and investment strategy.

Dollar-cost averaging does not assure a profit and does not protect against loss in declining markets. Such a plan involves continuous investment in securities regardless of the fluctuation of price levels of such securities. An investor should consider his or her financial ability to continue his or her purchases through periods of low price levels.

TAKE CONTROL OF YOUR RETIREMENT JOURNEY, SCHEDULE A CONSULTATION TODAY

DOWNLOAD OUR GUIDE

THE RETIREMENT INCOME ROADMAP